What is common between Merck, Sberbank, Krung Thai Bank, Midea Group, State Bank of India, Stanley Black and Decker, Ford Otosan, Olam International, DBS Group, Cielo, Rentokil Initial, Posco, China Telecom, and Unilever? Apart from being large global enterprises, they are also a part of the 100 Global Gems of Digital Enterprise list – the front runners in exploiting digital to transform and perform.

The 100 Global Gems of Digital Enterprise list was released by Coeus Age, a fast-growing research organization based out of India. The coveted list is part of a global research report titled ‘A Board’s Eye View of Digital in Enterprise’, conducted by Coeus Age between November 2018 and March 2019.

Gauging ‘Digital in Enterprise’

The aim of the research was to gauge the ‘digital in enterprise’ phenomenon in companies. For this Coeus Age scanned through reams of data to figure how digital had become part of the business strategy of companies. In all, 1,750 large enterprises from the Forbes 2000 list of 2018, across 19 industries and 60 sub industries, 6 continents, and 62 countries were covered. The research scored each enterprise on four dimensions and ten sub dimensions. The four dimensions were –Spread of Digital in the Narrative, Strategic Appreciation of Digital, Concrete Adoption of Digital and Support Environment for Digital. Each enterprise could obtain a maximum score of 30.

If Based in India –Click Here to Purchase; If Based outside of India – Click Here to Purchase

“This is a first of its kind list of top 100 Enterprises, as seen from the digital lens. Though ‘digital in enterprise’ is a nascent phenomenon, our study suggests that it is already a broad based one. It shall become more prominent over the next five to seven years”, said Dr Kapil Dev Singh, Principal Research Analyst and CEO, Coeus Age.

Diversity by Industry and Geography

The report reveals that the global gems of digital enterprise hailed from diverse geographies and industries. The list of 100 Global Gems of Digital Enterprise (GGODE) was obtained by arranging the enterprises by their respective Digital Scores. These enterprises are early and successful adopters of ‘digital in enterprise’ to transform and perform.

- Merck of Germany is at the top of the list followed by Sberbank of Russia. The third spot is occupied by 5 enterprises with a common score – Krung Thai Bank (Thailand), Midea Group (China), SEB SA (France), Siam Cement Group (Thailand), and State Bank of India (India).

- Another 6 with a common score occupy the fourth spot Schaeffler (Germany), Stanley Black & Decker (USA), DBS Group (Singapore), Banco Santandar (Spain), Novartis (Switzerland) and Naspers (South Africa)

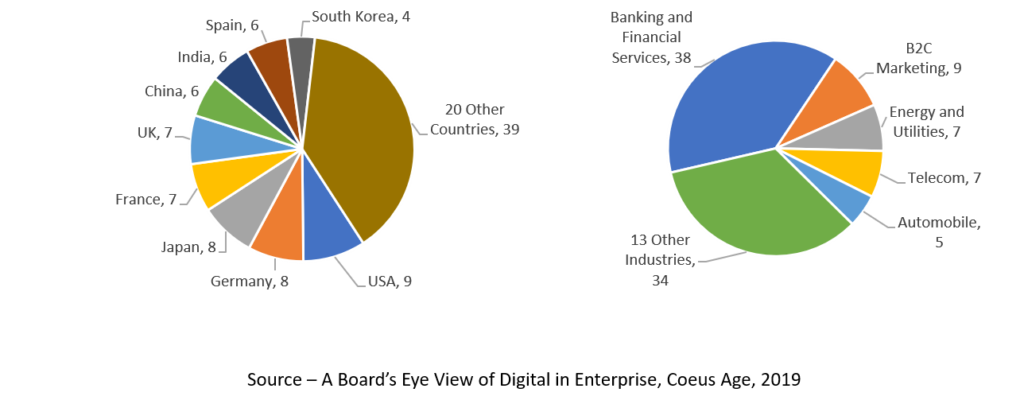

- Among the countries, USA leads the 100 GGODE list with 9 enterprises, followed by Germany and Japan (8 each); France and UK (7 each); Spain, China, and India (6 each), and Korea (4).

- However, continent-wise, Europe and Asia (excluding west Asia) lead the list with 40 enterprises each.

- In terms of industry verticals, Banking and Financial Services leads the list with 38 enterprises, followed by B2C Marketing (9), Energy & Utilities and Telecom (7 each) and Auto (5).

The list can also be seen by countries and industries.

- Itau Unibanco Holdings (BFS), Fineco Bank (BFS), Toyota Motors (Auto), ING Group (BFS), Etisalat (Telecom), and GlaxoSmithKline (Bio and Pharma) are leaders in Brazil, Italy, Japan, Netherlands, UK and Turkey.

- Rentokil Initial (UK), Larsen and Toubro (India), Red Electrica (Spain), Olam International (Singapore), Ceconomy (Germany) and Sompo (Japan) are leaders in the B2B, Construction, Energy and Utilities, Food and Beverages, Retail, and Insurance industries.

“Though the 100 Global Gems of Digital Enterprises are concentrated in few countries and industries, there is a broad representation across 29 countries and 18 industry verticals. This shows that over time, the ‘digital in enterprise’ phenomenon will become widespread as more and more company boards become conscious about its relevance and importance’, said Dr. Kapil Dev Singh.

What Makes Global Gems of Digital Unique?

What emerged from the study was that the leading digital enterprises of the world have some unique characteristics that set them apart from others. The research found the Global Gems of Digital Enterprise to have an explicitly stated big vision or dream about the way the future shall unfold.

For instance, Olam ‘reimagines global agriculture,’ Toyota ‘envisions a connected world,’ and Sberbank ‘strives for a global ecosystem.’

They see themselves playing a big role in crafting that dream, and there is a deep sense of purpose and the goal to be achieved. E.g., Merck is ‘passionate about discovering better drugs through cross border collaborations,’ Midea ‘wants to be a global leader,’ and Posco ‘aims at building smartness across the value chain.’ Not only is the dream lofty, it’s also firmly grounded. They, in no unequivocal terms, weave digital in their strategic discourse, how the new and emerging technologies such as big data analytics, machine learning, artificial intelligence, and internet of things shall be exploited to support the strategic route to realize the big dream. They have a broad-based adoption of a range of emerging digital technologies across multiple business domains for a business centric platform to emerge. This is over the traditional IT as defined in terms of infrastructure and applications such as ERP, CRM, eProcurement, SCM etc.

For the Gems of Digital Enterprise, it’s not digital per se that is important, but its strategic import that is more relevant. They give primacy to the quality of strategy, digital is just an important weapon in the arsenal, an enabler.

These enterprises are also transforming their enterprise through interventions such as culture change, leadership orientation, skill building, new structures of implementation and practicing clearly defined metrics and KPIs. Not only are they focussed on their enterprise but are equally active in building a greater enterprise, one which brings digital start-ups, R&D labs and academic institutions under their ambit for driving the innovation in the digital engine. E.g. Cielo ‘is busy nurturing, closer relationships with the ecosystem of innovation at universities, startups, and other companies,’ and Toyota ‘is running an innovation program Toyota Next.’”

Digital as the Cornerstone of a New Strategic Paradigm

“Enterprises are witnessing a new business paradigm, in which they will have to relentlessly create Small Windows of Competitive Advantage (SWOCA) to survive and thrive.

An insight that clearly emanates from the performance data of enterprises, measured in terms of year-on-year revenue growth, year-on-year net profit growth and the profit margin. When compared across four sets of enterprises (top 13, top 59, top 100 by digital score and all 656 sampled), there is no significant difference in the revenue growth and net profit margin, but there is a clear difference between their revenue growth figures. This indicates a direct and strong correlation between the digitals score and the net profit margin. The higher the digital score, the higher the net profit margin.

It hints at an emerging paradigm of business where it’s becoming difficult to grow revenues, given the high degree of disruption and the unwillingness of the customers to pay more even for better customer experience. This, coupled with increasing input costs is squeezing the margins. More and more industries are finding answers to this dilemma of falling revenues and growing costs by utilizing digital and tweaking their business models. E.g., banks are alluring customers to online banking and are using chat bots to address their queries.

Innovative Methodology

Coeus Age scanned, coded and analysed vast amount of content that is contained in annual reports of the large enterprises. A painstaking process that involved a framework creation, scanning and coding of content and analysis using the framework, took 12 man-months of efforts.

In terms of depth, Coeus Age analysts sifted through thousands and thousands of pages (330,000 to be precise) looking for the narrative around digital (and related aspects that make it) to decode the construct of ‘digital in enterprise’. In total 62,000 digital-related words were identified, and 3,771 chunks of qualitative content were analysed.

Coeus Age is a fast-growing research and consulting organization that develops deep and actionable insights for rekindling business growth. It helps the clients embrace a new growth paradigm in the age of digital disruption.

Coeus Age has always been the first mover in demystifying the construct of Digital Enterprise. It was the first in defining Digital Enterprise holistically (2014), highlighting the importance of Platform Thinking (2016), and discovering the Gems of Digital Enterprise in India (2017) and Gems of Digital India (eGovernance) (2017, 2018). In 2018, Coeus Age took a global stride by launching the initiative A Board’s Eye View of Digital in Enterprise and releasing the first list of 100 Global Gems of Digital Enterprise.

Coeus Age was started by Dr. Kapil Dev Singh, an industry analyst of high repute, who in his earlier stint headed IDC in India for a long 8 years. After moving out from IDC in 2010 and completing his doctorate in 2014, Dr. Singh focussed on spear heading research and consulting on Digital Enterprise.

Dr. Singh has authored several books during this period, notable ones being The Platform Thinking, LEADDDING, Thriving in a Data Economy, 51 Gems of Digital India, CIO Leading Change and Looking Inward.

www.coeusage.com, www.leaddding.com,www.maximumgovernance.com

—————————————————————————————————-

E.g. one of the state governments started an app based service to upload the pictures of garbage citizens may want to be cleared. The app is tagged with the time and location data to ensure that it is a genuine problem. It would trigger the process internally to ensure that someone comes and collects the garbage. The app can help track the time elapsed between the request was triggered and the garbage collected. The real test of the app shall happen when it can help close the loop by posting photos with time and location stamp post garbage clearing. The sheer volume of requests by the citizens has to be handled and each loop has to be closed. Similarly in case of citizens or citizen groups participating in planning, implementation and monitoring of e-governance services, the government machinery has to work closely with and respond to them. Does the government has the the capacity to do so?

E.g. one of the state governments started an app based service to upload the pictures of garbage citizens may want to be cleared. The app is tagged with the time and location data to ensure that it is a genuine problem. It would trigger the process internally to ensure that someone comes and collects the garbage. The app can help track the time elapsed between the request was triggered and the garbage collected. The real test of the app shall happen when it can help close the loop by posting photos with time and location stamp post garbage clearing. The sheer volume of requests by the citizens has to be handled and each loop has to be closed. Similarly in case of citizens or citizen groups participating in planning, implementation and monitoring of e-governance services, the government machinery has to work closely with and respond to them. Does the government has the the capacity to do so?